TORONTO, July 28, 2021 /PRNewswire/ - Golden Star Resources Ltd. (NYSE American: GSS) (TSX: GSC) (GSE: GSR) ("Golden Star" or the "Company") reports its financial and operational results for the three and six months ended June 30, 2021. All references herein to "$" are to United States dollars.

Q2 2021 HIGHLIGHTS:

- Q2 2021 production totaled 37.9 thousand ounces ("koz") from Wassa, at an all-in sustaining cost ("AISC") of $1,182 per ounce ("/oz"). H1 2021 production totaled 78.0koz at an AISC of $1,140/oz, and the Company remains on track to deliver on the recently revised production guidance of 145-155koz for 2021.

- The Wassa underground grade averaged 3.1 grams per tonne ("g/t") in Q2 2021, in line with the reserve grade and 4% higher than achieved in Q1 2021.

- Paste fill test work continued during the quarter with recent positive results supporting a second test stope currently in progress which, if successful, will lead to the restart of the planned filling schedule in Q4 2021.

- Q2 2021 saw continued investment in infill drilling and development at Wassa, ahead of planned future production expansion. Q2 2021 capital expenditure totaled $12 million ("m").

- Cash increased by $6.6m in Q2 2021 to total $72.7m at June 30, 2021, with net debt reducing to $31m.

- The senior secured credit facility with Macquarie Bank Limited (the "Macquarie Credit Facility") was restructured and upsized to a three-year $90m revolving credit facility ("RCF"), with $30m of undrawn liquidity. The amortization profile was also restructured, releasing $30m of liquidity in 2021 and 2022.

- The refinancing plus the cash on hand position Golden Star for the repayment of the 7% convertible debentures maturing in August 2021 (the "Convertible Debentures"). This deleveraging event will further strengthen the Company's balance sheet and deliver a lower cost of capital.

- In-mine exploration continued to deliver positive drill results adjacent to the current and planned reserve mining areas, with infill drilling now underway aimed at identifying mineral resources by the year end.

Table 1 – Q2 2021Performance Summary (Continuing Operations unless otherwise stated)

|

1. See "Non-GAAP Financial Measures" |

Q2 2021 |

Q2 2020 |

% change |

H1 2021 |

H1 2020 |

% change |

|

|

Production – Wassa |

Koz |

37.9 |

44.8 |

(15)% |

78.0 |

85.1 |

(8)% |

|

Production – Prestea (discontinued operation) |

Koz |

- |

5.9 |

(100)% |

- |

15.5 |

(100)% |

|

Total gold produced |

Koz |

37.9 |

50.6 |

(25)% |

78.0 |

100.6 |

(22)% |

|

Gold sold – Wassa |

Koz |

37.7 |

46.5 |

(19)% |

76.6 |

83.0 |

(8)% |

|

Gold sold - Prestea (discontinued operation) |

Koz |

- |

6.2 |

(100)% |

- |

15.2 |

(100)% |

|

Total gold sold |

Koz |

37.7 |

52.7 |

(28)% |

76.6 |

98.2 |

(22)% |

|

Average realized gold price (incl. Deferred Revenue) |

$/oz |

1,709 |

1,621 |

5% |

1,688 |

1,559 |

8% |

|

Cash operating cost per ounce - Wassa1 |

$/oz |

752 |

633 |

19% |

734 |

632 |

16% |

|

Cash operating cost per ounce - Prestea1 |

$/oz |

- |

2,292 |

(100)% |

- |

1,986 |

(100)% |

|

Cash operating cost per ounce - Consolidated1 |

$/oz |

752 |

827 |

(9)% |

734 |

842 |

(13)% |

|

All-in sustaining cost per ounce - Wassa1 |

$/oz |

1,182 |

957 |

23% |

1,140 |

958 |

19% |

|

All-in sustaining cost per ounce - Prestea1 |

$/oz |

- |

2,910 |

(100)% |

- |

2,471 |

(100)% |

|

All-in sustaining cost per ounce - Consolidated1 |

$/oz |

1,182 |

1,186 |

-% |

1,140 |

1,193 |

(4)% |

|

Gold revenues |

$m |

64.4 |

75.4 |

(15)% |

129.4 |

129.5 |

- |

|

Adj. EBITDA1 |

$m |

26.0 |

36.4 |

(28)% |

53.3 |

57.6 |

(8)% |

|

Adj. income/share attributable to shareholders - basic1 |

$/share |

0.05 |

0.10 |

(50)% |

0.09 |

0.12 |

(25)% |

|

Cash provided by operations before working capital |

$m |

23.2 |

34.9 |

(34)% |

46.5 |

52.1 |

(11)% |

|

Changes in working capital and taxes paid |

$m |

(10.3) |

(4.0) |

(158)% |

(23.3) |

(13.5) |

(73)% |

|

Net cash used in investing activities |

$m |

(10.4) |

(9.6) |

(8)% |

(23.2) |

(22.0) |

(5)% |

|

Net cash provided by financing activities |

$m |

4.2 |

(5.6) |

175% |

11.9 |

(5.5) |

316% |

|

Free cash flow 1 |

$m |

2.4 |

21.4 |

(89)% |

- |

16.5 |

(100)% |

|

Cash |

$m |

72.7 |

45.1 |

61% |

72.7 |

45.1 |

61% |

|

Net Debt |

$m |

31.0 |

56.0 |

(45)% |

31.0 |

56.0 |

(45)% |

Andrew Wray, Chief Executive Officer of Golden Star, commented:

"Our primary objectives for H1 2021 were to continue positioning the business for future production growth, as well as to be able to address the repayment of the $51.5m Convertible Debentures in August 2021. With the increase in the cash position to $72.7m during the quarter and the successful refinancing of the Macquarie Credit Facility, we now have adequate liquidity to be able to cash settle the Convertible Debentures on maturity.

Following the recent revision of our 2021 guidance, our key operational focus is the completion of the commissioning of the paste fill plant by the end of the year. Recent paste strength test work has yielded positive results and supports the advancement of a second test stope during Q3 2021. We will issue further updates through H2 2021 as we progress towards our target of production from secondary stopes in 2022.

While the paste fill test work progresses, we are also continuing to make operating changes aimed at unlocking further improvements in development rates in order to improve the operational flexibility. This work enabled the decline development to reach the 495 level during the quarter. This milestone was critical in providing the operations with more flexibility - this opens up the new production areas needed to provide access to the primary stopes that were originally planned for 2022 and are now being brought forward to partially replace the secondary stopes that were deferred as a result of the ongoing paste fill strength test work.

The step up in the investment in exploration in 2021 is yielding positive results, particularly the in-mine program where we are now reallocating resources from regional targets to carry out additional in-fill drilling to delineate resource in targets proximal to existing and planned reserve infrastructure.

As we go into H2 2021, the repayment of the convertible debenture represents another significant step in the restructuring and strengthening of our balance sheet while the operational focus on full commissioning of paste fill activities and consistent delivery of the increased development metres will return the operation to where we planned it to be to deliver further growth in 2022 and beyond."

Q2 2021 RESULTS WEBCAST AND CONFERENCE CALL

The Company will conduct a Q2 2021 results conference call and webcast on Thursday July 29, 2021 at 10.00 am ET.Toll Free (North America): +1 888 390 0546

Toronto Local and International: +1 416 764 8688

Toll Free (UK): 0800 652 2435

Conference ID: 98666950

Webcast: https://produceredition.webcasts.com/starthere.jsp?ei=1477518&tp_key=0b1e14f35eFollowing the conference call, a recording will be available on the Company's website at: www.gsr.com.

KEY EVENTS – Q2 2021

Wassa Operational Performance and Infrastructure Investment

- The mining rate averaged 3,963 tonnes per day ("tpd") in Q2 2021, representing a 10% decrease on the 4,418tpd achieved in Q2 2020 and 12% lower than the mining rate of 4,499tpd achieved in Q1 2021 driven predominantly by an enforced change in the mine plan due to stoping constraints caused by lower than planned development rates.

- Underground mined grade averaged 3.1g/t, in line with the underground reserve grade of 3.1g/t and 4% higher than the grade achieved in Q1 2021.

- Processing of low-grade stockpiles continued during Q2 2021, given the continued strength of the gold price. This initiative, which utilizes latent capacity in the process plant without compromising gold recovery rates, contributes additional cash flow, albeit at a slightly higher AISC than achieved by the underground mine. This initiative contributed 5koz of production during Q2 2021.

- Investment in infrastructure continued throughout Q2 2021 to provide additional mining flexibility with the objective of increasing mining rates. Capital expenditure at Wassa totaled $12m during Q2 2021, including capitalized drilling of $1.9m.

- Operational improvements and recruitment of additional jumbo operators has seen an increase in development rates over the second half of the quarter, with June seeing rates in line with plan and representing a 15% increase compared to 2020. During the quarter, decline development reached the 495-level, access and level development has commenced bringing on new development and production areas into the mine plan for H2 2021. These stopes were originally planned for 2022 and will be brought forward to replace some of the secondary stope material delayed due to the delay in the completion of the paste plant commissioning process.

Paste Fill Commissioning Update

- The Paste fill plant commissioning process started in Q1 2021, following the completion of the plant construction in Q4 2020. As previously announced, the commissioning was delayed by some quality assurance testing returning lower than expected fill strengths in the test stope in April 2021.

- As a result, the test work program has been extended. The Company is working in collaboration with Minefill Services and the University of Mines and Technology in Tarkwa, Ghana. Core samples for the initial test stope have been obtained and are being tested in parallel with further test work on the mix design. Additional samples have now arrived in Australia for confirmatory testing and mix design test work. Recent test results, particularly at a higher cement content of 7-10%, have shown results that support progression of the commissioning process onto filling of a second test stope.

- The second test stope has been identified and is currently progressing through the production phase ahead of filling, which is anticipated to occur during Q3 2021. The stope will be tested with a 10% cement blend for maximum fill strength, while off-site mix design optimization and test work continue. Should this test work return satisfactory strength results, as expected, the Company anticipates re-commencement of the filling schedule in Q4 2021 allowing for production from secondary stopes, as previously planned, in 2022.

COVID-19 PANDEMIC

- Ghana experienced a slight increase in COVID-19 cases in Q2 2021. A total of 5,953 positive cases had been confirmed in the Western Region, where the Wassa mine is located, of which 23 were active cases as at June 30, 2021, an improvement over the previous quarter. During Q2 2021, Wassa experienced 10 suspected COVID-19 cases with six confirmed cases and two pending results as at quarter end.

- During 2021, the COVID-19 pandemic has impacted the availability of our expatriate operators. This resulted in lower than planned development rates being achieved, as reported in the Q1 2021 results and the recent paste fill plant commissioning update. The Company is investing in additional resources and has made changes to our operating structures to mitigate the ongoing impact of the COVID-19 pandemic on development rates.

- Supply chains for the shipment of dore to the refinery and for the key consumables, including cyanide, lime, grinding media, fuel, and lubricants, have remained intact throughout the pandemic. All supply chains are being continually monitored and alternative suppliers have been identified for essential supply chains.

Safety and Health

- In June 2021, two employees at the Wassa mining operations suffered minor injuries. Both employees are undergoing medical treatment and review with diagnoses of potential for full recovery. Reflecting these incidents, the all-injury frequency rate ("AIFR") of the continuing operations as at June 30, 2021 was 2.91 and the total recordable injury frequency rate ("TRIFR") was 0.97, based on a 12-month rolling average per million hours worked. This compares to the continuing operations AIFR of 3.57 and TRIFR of 0.54 as at June 30, 2020.

Restructuring and Upsizing of the Macquarie Credit Facility

- On May 31, 2021, the Company announced the restructuring and upsizing of the Macquarie Credit Facility to a three-year RCF. The capacity of the RCF has been upsized by $20 million to $90 million, which created $30 million of liquidity over and above the drawn balance of $60 million.

- The restructuring also removed the $5 million quarterly capital repayment amortization profile which was due to come into effect in September 2021 if the Macquarie Credit Facility was fully drawn, or March 2022 if the current $60 million drawn amount was sustained. Therefore, this released a further $10 million of liquidity in 2021 and $20 million in 2022.

- The capacity of the RCF will remain at $90 million to June 30, 2023, when it steps down to $50 million until maturity on June 30, 2024. The term of the RCF and the step down in the capacity will be reviewed annually and could be further extended, subject to the successful conversion of mineral resources to mineral reserves through the planned infill drilling program.

Gold Hedges

- As a condition of amending the Macquarie Credit Facility, the Company extended its gold price protection hedging program into the first half of 2024 by entering into zero cost collars with Macquarie Bank on an additional 84,375 ounces.

- This brought the total hedged position to 150,000 ounces as at June 30, 2021, maturing at a rate of 12,500 ounces per quarter from September 30, 2021 to June 30, 2024.

- The hedging program now covers 25-30% of the forecast production during the current term of the RCF. All hedges have a floor of $1,600/oz and an average ceiling of $2,171/oz in 2021 and $2,179/oz in 2022, and a flat ceiling of $2,115/oz in 2023 and 2024.

At The Market Equity Program

- On October 28, 2020, the Company entered into an at-the-market equity distribution program (the "ATM Program") with BMO Capital Markets Corp. ("BMO") relating to Golden Star common shares pursuant to a sales agreement (the "Sales Agreement"). In accordance with the terms of the Sales Agreement, the Company may distribute shares of common stock having a maximum aggregate sales price of up to $50 million from time to time through BMO as agent for the distribution of shares or as principal. The proceeds from the ATM Program will be used for discretionary growth capital at Wassa, exploration, general corporate purposes and working capital.

- A total of 4,220,213 shares of common stock had been sold under the Sales Agreement up to June 30, 2021, generating net proceeds of $13.8m, of which $5.2m was generated in Q2 2021.

Changes to the Board of Directors

- Karen Akiwumi-Tanoh and Gerard De Hert were elected as directors of the Company at the annual general meeting on May 6, 2021 (the "AGM"). Robert Doyle retired as a director of the Company after the AGM in line with Golden Star's board of directors (the "Board") mandate of a maximum term limit of 10 years for directors. Mona Quartey replaced Mr. Doyle as chair of the audit committee of the Board.

Sale of Prestea - Deferred Consideration Amendment Agreement

- On September 30, 2020, the Company completed the sale of its 90% interest in Prestea to Future Global Resources Limited ("FGR") pursuant to a share purchase agreement (the "SPA") for the sale by Golden Star's wholly owned subsidiary, Caystar Holdings ("Caystar"), and the purchase by FGR of all the issued and outstanding share capital of Bogoso Holdings ("Bogoso"), the holder of 90% of the shares of GSBPL, for a deferred consideration of $34.3 million guaranteed by Blue International Holdings ("BIH"), a major shareholder of FGR, which, prior to the amendments to the SPA as described below, was payable by FGR to Golden Star in the following tranches:

- $5 million in cash to be paid on the earlier of (i) the date at which FGR puts in place a new reclamation bond with the Environmental Protection Agency of Ghana (the "EPA") in relation to Prestea, and (ii) March 30, 2021;

- $10 million in cash and the net working capital adjusted balancing payment (as described in the SPA) which as at the date hereof amounts to approximately $4.3 million, to be paid on July 31, 2021; and

- $15 million in cash to be paid on July 31, 2023.

SPA Amendments

- On March 28, 2021, the Company and Caystar, entered into an agreement with FGR and BIH, to amend the SPA to account for deferred consideration conditions. The staged payments that form the deferred consideration, as outlined in the SPA, were reprofiled such that (i) the $5 million that was originally due on March 30, 2021 and (ii) the $10 million that was originally due on July 31, 2021, each became payable on May 31, 2021.

- On May 31, 2021, the Company and Caystar, entered into a second amending agreement with FGR and BIH, to further amend the SPA. The staged payments that form the deferred consideration were reprofiled to allow time for FGR to complete ongoing financing transactions and the environmental bonding process for Bogoso-Prestea. Pursuant to this second amendment to the SPA, the deferred consideration payments fall due as follows:

- the $15 million payment that was due on May 31, 2021 must be paid by no later than July 16, 2021; and

- an amount of approximately $4.6 million (comprised of the working capital balancing payment of approximately $4.3 million and fees of approximately $0.3 million for services provided by Caystar to FGR pursuant to a transition agreement dated September 30, 2020) must be paid by no later than July 31, 2021.

- As of the date hereof, FGR has defaulted on its obligation to pay Caystar $15 million by no later than July 16, 2021. FGR has claimed that it is entitled to set-off its obligation to make such payment under the SPA, as amended, as a result of various alleged breaches of the SPA, a claim which Golden Star and Caystar believe to be completely without merit. Caystar has also demanded that FGR pay the amount of $15 million pursuant to the guarantee made by BIH in the SPA. In the event payment is not received from BIH, Golden Star and Caystar are evaluating all available avenues of recourse in order to seek full recovery of amounts owed by FGR under the SPA.

Severance Claim

- On September 15, 2020, certain employees of Golden Star (Bogoso/Prestea) Limited, which subsequently changed its name to FGR Bogoso Prestea Limited ("FGRBPL") initiated proceedings before the courts in Ghana, claiming that the completion of the transaction contemplated by the SPA would trigger the termination of their existing employments, entitling them to severance payments (the "Severance Claim"). Caystar exercised its right under the SPA to assume control of the Severance Claim and legal counsel was retained on behalf of FGRBPL to defend the claim. No employment contracts were severed, amended or modified upon the completion of the sale transaction on September 30, 2020 and FGRBPL (owned by FGR since September 30, 2020) continued to operate with existing employment contracts and contractual terms being honored.

- On September 22, 2020, FGRBPL filed an application in court for an order striking out the plaintiffs' statement of claim for lack of standing or capacity and disclosing no reasonable cause of action. On February 16, 2021, the court ruled in favor of FGRBPL that the plaintiffs' pleadings disclosed no reasonable cause of action and were therefore frivolous, vexatious, and scandalous. Accordingly, the plaintiffs lacked the requisite standing or capacity to institute the action.

- On March 26, 2021, the plaintiffs filed a notice of appeal. As of the date hereof, the record of appeal is being transmitted from the High Court of Ghana to the Court of Appeal of Ghana. Notwithstanding the foregoing, FGR has entered into a settlement agreement with the plaintiffs in respect of the Severance Claim and it is not certain how such settlement by FGR will impact the pending appeal proceedings.

Energy Management and Climate Change

- A business-wide energy review was conducted at Wassa in June 2021 in the first stage of updated energy management planning at the business following the successful commissioning of the Genser natural gas power station. The review marks the first stage in establishing a baseline for the operation's proposed new energy mix. Evaluation of the identified energy opportunities will inform management on the marginal abatement cost curve for the business and in turn potential energy efficiency improvement, emission reduction and cost savings to be realized. These and other initiatives form part of the wider climate change management strategy of the Company.

Golden Star Oil Palm Plantations investment by Royal Gold

- On April 20, 2021, Golden Star Oil Palm Plantations Limited ("GSOPP"), a wholly-owned non-profit subsidiary of the Company, and RGLD Gold AG ("RGLD"), a wholly-owned subsidiary of Royal Gold, Inc. ("Royal Gold"), entered into an agreement providing for Royal Gold's investment in the oil palm plantations initiative, Golden Star's award-winning flagship sustainability project.

- In consideration of the long-standing relationship with the Wassa mine, and by extension the Wassa operation's host communities, Royal Gold has committed to provide financial support for the activities of GSOPP that benefit the Wassa operational communities through an annual contribution of $150,000 during each of the next five years. Royal Gold made its first contribution of $150,000 to GSOPP in April 2021. The investment will be used to accelerate development of the Company's innovative sustainability initiative which is aimed at creating sustainable alternative livelihoods, bringing additional economic stimulation and a legacy of community development to the region. The proceeds will support the further development of palm oil plantations around Wassa as well as activities to grow GSOPP including assessment of downstream processing opportunities.

- GSOPP is Golden Star's flagship sustainability and social enterprise initiative. It develops and operates oil palm plantations in communities proximate to the Company's gold mining operations, located in the Western Region of Ghana, for the benefit of members of the host communities. The program commits to ensuring that there is zero deforestation during the creation of a high value agribusiness on former subsistence farms and land that has previously been used for mining activities. Since its inception in 2006, GSOPP has developed plantations on over 1,500 hectares of land, which support over 700 families at levels of yield three times the small holder average in Ghana. The activities of GSOPP also align with the Company's wider sustainability goals of establishing high value post-mining land uses, self-funding revegetation and creation of biomass to act as a carbon sink to offset operational emissions.

2020 Corporate Responsibility Report

- The Company published its 2020 Corporate Responsibility Report on April 30, 2021. The report has been prepared in accordance with the Global Reporting Initiative Standards (Core option), the United Nations Global Compact reporting requirements, and the Sustainability Accounting Standards Board's ("SASB") Metals and Mining Sustainability Accounting Standard. The report and an ESG investor presentation are available on the Company's website at: www.gsr.com/responsibility.

- Key highlights of the report include:

- Leading practices in the management of the COVID-19 pandemic resulted in minimal impact to production and, more importantly, no lives lost to COVID-19 and limited serious health outcomes across the workforce.

- Sustained improvement in injury frequency rates across the Company was marred by a fatal incident at Prestea in March 2020.

- Wassa was recognized as the safest mine in Ghana, receiving the Best Performer in occupational health and safety at the Ghana Mining Industry Awards.

- Golden Star continues its leading practice performance in malaria prevention, with 2020 recording the lowest case rates and days lost to malaria on Company record.

- The Company achieved 100% conformance with its statutory monitoring program requirements and above 99% alignment to relevant quality standards.

- Consistent with our Inclusion and Diversity Policy launched in March 2020, the Company maintained its high rates of local content, with 99% of the workforce in Ghana being Ghanaian nationals and 59% of the workforce hailing from local host communities.

FULL YEAR 2021 PRODUCTION, COST AND CAPITAL EXPENDITURE GUIDANCE

As previously highlighted in the Q1 2021 results press release, the commissioning process for the new paste fill plant returned lower than expected strength test results in the first test stope. This outcome resulted in a delay to the commissioning process. Further test work and analysis is being carried out to ensure that the paste plant produces material at the required strength to enable safe mining operations and successful pillar extraction.

This test work is ongoing and positive progress has been made, with the most recent strength test results more aligned with the design parameters. A second commissioning test stope has been identified and will be completed in Q3 2021. This will be tested with a higher cement content at 10%, and, should it meet the required design strength requirements, as expected, then filling can recommence in Q4 2021.

The delay to the completion of commissioning of the paste plant impacts 21% of the Company's planned ore tonnes for 2021. This impact has been exacerbated by the lower than planned development metres primarily due to operator availability caused by issues related to the COVID-19 pandemic. The resolution of both issues is on track for completion in 2021. However, resequencing the mine plan for the remainder of the year means that the volume of ore available will be lower and at a slightly lower grade than initially planned due to the deferral into 2022 of the higher-grade secondary stopes.

As a result, production guidance for 2021 has been reduced to 145koz to 155koz, and the AISC guidance range has increased to $1,150/oz to $1,250/oz, which is driven predominantly by lower production volumes and anticipated cost inflation.

The capital expenditure guidance range is unchanged at $45 million to $50 million. While the overall budget is consistent, the sustaining capital guidance has been increased due to the increased investment in development and the tailings storage facility ("TSF") expansion project. The expansion capital guidance has been reduced with some ventilation capital deferred from Q4 2021 to early 2022. This deferral is not expected to have an impact on the short to mid-term mine plans.

The $14 million exploration budget for the year is broadly in line with the previous guidance, albeit with an increase in the allocation of spend to the up-dip and down-dip, in-mine, drilling targets that have delivered positive results so far this year.

Table 2: FULL YEAR 2021 Production and Cost Guidance

|

Unit |

Updated 2021 |

2021 Guidance |

|

|

Production and cost guidance |

|||

|

Gold Production |

(koz) |

145-155 |

165-175 |

|

Cash Operating cost1 |

($/oz) |

750-800 |

660-700 |

|

AISC1 |

($/oz) |

1,150-1,250 |

1,000-1,075 |

|

Capital expenditure guidance |

|||

|

Sustaining Capital2 |

($m) |

32-35 |

26-28 |

|

Expansion Capital2 |

($m) |

13-15 |

19-22 |

|

Total Capital Expenditure |

($m) |

45-50 |

45-50 |

|

Capitalized exploration |

($m) |

8 |

4 |

|

Expensed exploration |

($m) |

6 |

11 |

|

Total Exploration |

($m) |

14 |

15 |

|

Total Capital and exploration expenditure |

($m) |

59-64 |

60-65 |

|

Notes: |

|

1. See "Non-GAAP Financial Measures". 2. Expansion capital are those costs incurred at new operations and costs related to major projects at existing operations where these projects will materially increase production. All other costs relating to existing operations are considered sustaining capital. |

SUMMARY OF CONSOLIDATED OPERATIONAL RESULTS – Q2 2021

Wassa Operational Overview

Gold production from Wassa was 37.9koz in Q2 2021, 15% lower than the 44.8koz produced during Q2 2020. This decrease was driven by slower than planned development rates, which resulted in lower underground ore tonnes. The lower mined volumes were in part offset by higher processing volumes driven by low-grade stockpile tonnes which had an adverse impact on the overall processed grade.

Recovery

The recovery was 95.5% for Q2 2021, remaining consistent with Q1 2021, and demonstrating robust performance despite the volume of low-grade stockpiles processed in the period.

Wassa Underground

Production – The Wassa underground mine ("Wassa Underground") produced 33.3koz of gold (approximately 88% of Wassa's total production) in the second quarter of 2021. This compared to 42.4koz produced in Q2 2020 which was a strong comparative period with both higher mining rates and grades.

Mining rate - Wassa Underground mining rates averaged 3,963tpd in Q2 2021, 10% lower than the mining rate of 4,418tpd achieved in Q2 2020 and 12% lower than the 4,499tpd achieved in Q1 2020. The reduction in the mining rate resulted from an enforced change in the mine plan due to stoping constraints caused by lower than planned development rates.

Grade - The underground grade averaged 3.1g/t during the quarter, slightly higher than achieved in Q1 2021 and in line with the reserve grade.

Wassa Main Pit/Stockpiles

Low grade stockpiles from the Wassa main pit of 216.0kt with an average grade of 0.66 g/t were blended with the Wassa Underground ore during Q2 2021 which yielded 4.7koz of gold, compared to 2.4koz in Q2 2020. There has been no material impact on recoveries and the Company will continue to opportunistically process low grade stockpiles in 2021 should the current gold price environment continue.

Unit costs

The unit cost performance remained robust during Q2 2021. The mining unit cost of $40.3/t of ore mined was 29% higher than in Q2 2020 as a result of the lower mining rate. Higher plant throughput as a result of the increased volume of low-grade stockpile material treated benefited processing costs which totaled $16.1/t of ore processed, some 8% lower than the $17.5/t achieved in Q2 2020.

Costs per ounce

Cost of sales per ounce increased 21% to $1,033/oz for Q2 2021 compared to Q2 2020 due to lower production volumes, increased mine operating costs and increased depreciation costs, which was in part offset by the operating costs to metal inventory credit.

Cash operating cost per ounce increased 19% to $752 for Q2 2021 compared to Q2 2020 mainly due to:

- Lower production volumes translating into lower sales ounces

- Higher underground mining costs associated with increased grade control drilling

- Higher labor costs driven by year-on-year inflationary increases

- Increased fuel costs as Q2 2020 benefited from a temporary government subsidy (COVID-19 related) on power costs that has not continued into the current period

AISC increased 23% to $1,182/oz in Q2 2021 compared to Q2 2020 due to a combination of:

- Lower production and sales volumes

- Increased cash operating costs as outlined above

- Higher sustaining capital expenditure

- Increased higher cost stockpile tonnes processed

Capital expendituresCapital expenditures at Wassa for Q2 2021 totaled $12m, in line with expenditure in Q2 2020. The Wassa management team continued to focus its efforts on critical development spend in order to support the medium-term growth of the underground operation including:

- Sustaining capital on capitalized underground development activities of $3.6m (Q2 2020: $3.8m) and expansion of the TSF of $3.3m (Q2 2020: $ nil).

- Capitalized exploration drilling of $1.9m (Q2 2020: $0.1m) mainly related to the Wassa up-dip and down-dip extensions, development costs for increased future production of $0.8m (Q2 2020: $0.8m) and diamond drilling decline on 570 Level of $0.7m (Q2 2020: $ nil) where two drill rigs were focused on inferred to indicated resource conversion to the south of the existing reserves in the area covered by the preliminary economic assessment (the "PEA Area") included in the Wassa Technical Report.

- $3.7m was incurred on the commissioning of the paste fill plant project in Q2 2021.

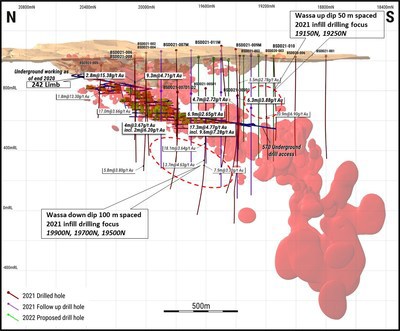

Wassa underground infill drilling

For Q2 2021, the Wassa Underground drilling program completed 20,906 metres of diamond core drilling, for a total drilling and assay cost of $2.9m for the period.

Initially, three underground drill rigs focused on converting existing indicated resources to measured resources inside the mine. An additional two drills focused on converting inferred resources to indicated resources in the PEA Area. By mid-May, the drilling activities changed focus, with all five drills converting indicated resources to measured resources inside the mine.

- Reserve infill drilling - The Q2 2021 resource infill drilling program focused on the conversion of indicated resources to measured resources, with a total of 16,661 metres drilled in Q2, for a total cost of $2.2m. This program is expensed and is anticipated to reach approximately 44,000 metres by year end.

- Infill drilling of the Southern Extension (PEA Area) - During Q2 2021, the program focused on the conversion of inferred resources to indicated resources in Panel 4. Drilling totaled 4,245 metres for a cost of $0.7m. This program is capitalized and is expected to total around 30,000 metres during 2021. This drilling takes place from the 570 diamond drill decline.

EXPLORATION

During Q2 2021, $3.3m was invested in exploration at Wassa and the regional Hwini Butre and Benso ("HBB") concessions, of which $1.9m of Wassa in-mine exploration was capitalized and the balance of $1.4m was expensed.

Wassa – In-mine exploration

During Q2 2021, three surface drill rigs continued the testing of targets down-dip of the existing Wassa reserve. The first phase of drilling on an initial 200 metre spaced fences was completed towards the end of the quarter and has been followed by in-fill drilling to reduce the spacing of the initial program to 100 metres and 50 metres for down-dip and up-dip programs respectively, in areas where results have shown extensions of the mineralization of known resources. A total of five holes were completed for 4,827 metres during Q2 2021, bringing the year-to-date drilling to 11,175 metres.

The following table presents a summary of the results of exploration drilling at Wassa during Q2 2021:

Table 3: Q2 2021 Exploration Drilling Results Identify Extensions of the Wassa Underground Mineralization

|

Hole ID |

Azimuth |

Dip |

From |

To |

Drilled Width |

Estimated |

Grade Au |

Drilling |

|

BSDD21-006 |

89.2 |

-64.2 |

101.7 |

104.7 |

3 |

3 |

6.33 |

Down-dip |

|

BSDD21-006 |

90.8 |

-65 |

176 |

179 |

3 |

2.8 |

15.38 |

Down-dip |

|

BSDD21-006 |

91.9 |

-65.1 |

315.8 |

319.8 |

4 |

2.1 |

2.51 |

Down-dip |

|

BSDD21-006 |

91.4 |

-65.3 |

364.5 |

368 |

3.5 |

1.8 |

2.25 |

Down-dip |

|

BSDD21-006 |

90.1 |

-66.1 |

406.1 |

409 |

2.9 |

1.5 |

2.01 |

Down-dip |

|

BSDD21-007M |

88.1 |

-55.9 |

535 |

553 |

18 |

17.3 |

4.77 |

Down-dip |

|

Including |

88.1 |

-55.9 |

536 |

546 |

10 |

9.6 |

7.28 |

Down-dip |

|

BSDD21-007M |

88 |

-56.1 |

629 |

631.5 |

2.5 |

2.4 |

3.22 |

Down-dip |

|

BSDD21-008 |

92 |

-72.6 |

176.3 |

185.7 |

9.4 |

9.3 |

4.71 |

Down-dip |

|

BSDD21-007D1 |

88 |

-71.2 |

183 |

190 |

7 |

6.9 |

2.65 |

Down-dip |

|

BSDD21-009M |

94.3 |

-63.1 |

299 |

307 |

8 |

6.8 |

1.49 |

Down-dip |

|

BSDD21-009M |

92.2 |

-63.6 |

374 |

383 |

9 |

4.7 |

2.72 |

Down-dip |

|

BSDD21-009M |

73.5 |

-68.1 |

741 |

746 |

5 |

3.8 |

1.23 |

Down-dip |

|

BSDD21-009M |

66.1 |

-69 |

786 |

788 |

2 |

1.5 |

2.04 |

Down-dip |

|

BSDD21-009M |

61.5 |

-70.4 |

833.8 |

838.8 |

5 |

3.7 |

1.96 |

Down-dip |

")

Down-dip infill drilling to reduce drill fence spacing to 100 metres is expected to continue in Q3 2021 between sections 19200N and 20000N. The results gathered during Q2 2021 included the following highlights:

- BSDD21-008 (down-dip) on section 20075N, intercepting 9.3 metres at 4.71g/t, which is in line with the western limb extension of the 242 mineralized structure and will require further follow up drilling.

- BSDD21-007M (down-dip) intercepting 17.3 metres at 4.77 g/t, This intersection is further confirmation that the B Shoot Hanging Wall mineralization extends along strike of the current reserve therefore warranting further drilling down-dip.

- BSDD21-007D1 (down-dip) intercepting 6.9 metres at 2.65 g/t c.50 metres down dip of BSDD21-007M, which intersected 17.3m grading 4.77 g/t. Further step-out drilling will be required to test down-dip extension of mineralization below the existing reserve as there is no deep drilling to the west of the current drill hole.

Exploration programs for Q3 2021 are planned to continue with infill drilling of the up-dip and down-dip extensions of mineralization, reducing the initial 200-metre spacing to 100 metres for the down-dip program and 50 metres for the up-dip program. The down-dip infill program will focus between 19400N and 2000N, where zones of mineralization have been intersected. The up-dip follow up program designed to close-up drill spacing to 50 metres will be conducted from 19150N to 19250N. This tighter drill spacing has been plann-ned around the significant intersection on section 19200N, BSDD20-003 which intersected 20.9 metres grading 6.9 g/t. Should the closer drill spacing on this target continue to intersect significant widths and grades, then additional resources close to the existing underground infrastructure could be added.

Wassa – Near-mine exploration

The diamond ("DD") and reverse circulation ("RC") drill testing of three additional targets outside of the main Wassa deposit, commenced in Q2 2021. These targets, testing extensions of mineralization beneath the mined and back-filled open pits of South Akyempim ("SAK"), Mid East ("ME") and Dead Man Hill ("DMH") and are outside of the forest reserve and required no forest entry permitting to conduct exploration work. Meanwhile, an application for a forest entry permit has been submitted to the Ministry of Lands and Natural Resources of Ghana to conduct follow up drilling on the remaining four targets inside the forest reserve. Planned first phase drilling (RC/DD) at ME and DMH have completed with drilling currently ongoing at SAK. A total of seven holes were drilled for 2,394 metres during Q2 2021. In addition to the RC and DD on other targets, initial air core drilling of a soil anomaly south east of the Wassa trend was also conducted with 59 holes totaling 2,365m being completed.

Table 4: Q2 2021 Exploration Drilling Results - Wassa Near-Mine

|

Hole ID |

Azimuth |

Dip |

From |

To |

Drilled Width |

Estimated |

Grade Au |

Drilling |

|

SAKDD21-001 |

275.9 |

-59.3 |

318.0 |

321.0 |

3.0 |

2.1 |

2.64 |

Below Pit |

|

SAKDD21-002 |

269.9 |

-55.5 |

250.0 |

253.0 |

3.0 |

2.1 |

1.64 |

Below Pit |

|

SAKDD21-002 |

269.9 |

-55.5 |

256.7 |

257.4 |

0.7 |

0.5 |

5.26 |

Below Pit |

|

SAKDD21-002 |

270.2 |

-55.4 |

266.0 |

268.0 |

2.0 |

2.0 |

2.52 |

Below Pit |

|

MEDD21-001 |

53.3 |

-47.4 |

57.0 |

60.0 |

3.0 |

2.9 |

2.76 |

Below Pit |

|

MEDD21-001 |

53.8 |

-46.7 |

198.0 |

204.0 |

6.0 |

5.9 |

2.37 |

Below Pit |

|

MEDD21-001 |

53.9 |

-46.7 |

210.4 |

218.4 |

8.0 |

7.8 |

2.07 |

Below Pit |

|

MEDD21-002 |

28.4 |

-59.3 |

110.0 |

112.0 |

2.0 |

2.0 |

2.40 |

Below Pit |

|

MEDD21-002 |

22.8 |

-58.7 |

258.3 |

260.5 |

2.2 |

1.9 |

1.45 |

Below Pit |

|

MEDD21-002 |

22.8 |

-58.7 |

267.0 |

270.0 |

3.0 |

2.6 |

1.26 |

Below Pit |

|

MEDD21-002 |

23.0 |

-58.7 |

272.4 |

275.4 |

3.0 |

2.6 |

2.78 |

Below Pit |

Drilling beneath the mined out pits of ME and SAK generally intersected mineralized structures at target areas as projected but at weaker grades beyond existing drilling. Follow up drilling will be designed after comprehensive evaluation of the results for the first phase drilling which will be completed in Q3 2021.

HBB – Regional exploration

Exploration work testing 11 prioritized targets along the HBB trend continued in Q2 2021. Community sensitization and crop compensation have been completed for four of the southern targets. Air core drilling was successfully undertaken at four of the target areas, namely Seikrom, Guadium, Kwahu and Abada South, with a total of 125 holes for 4,902 metres being completed. Drilling and crop compensation negotiations, as well as drill pad and access construction for the remaining targets, are ongoing. Line cutting ahead of the ground geophysics programs has progressed well and the geophysics crews are scheduled to arrive in Q3 2021.

Table 5: Q2 2021 Exploration Drilling Results - Regional Exploration - HBB

|

Hole ID |

Prospect |

Northing |

Easting |

From |

To (metres) |

Drilled |

Grade |

|

SEKAC21-001 |

Seikrom |

36133.47 |

177840.21 |

3.0 |

12.0 |

9.0 |

1.09 |

|

SEKAC21-001 |

Seikrom |

36133.47 |

177840.21 |

27.0 |

36.0 |

9.0 |

1.14 |

|

SEKAC21-005 |

Seikrom |

36068.35 |

177739.60 |

0.0 |

3.0 |

3.0 |

1.34 |

|

SEKAC21-023 |

Seikrom |

36135.51 |

177835.63 |

9.0 |

15.0 |

6.0 |

0.98 |

|

GUAAC21-001 |

Guadium |

46032.98 |

177259.73 |

3.0 |

9.0 |

6.0 |

0.80 |

|

GUAAC21-007 |

Guadium |

45833.17 |

177271.03 |

54.0 |

57.0 |

3.0 |

2.37 |

|

GUAAC21-010 |

Guadium |

45833.13 |

177157.75 |

21.0 |

27.0 |

6.0 |

1.20 |

|

GUAAC21-013 |

Guadium |

45436.60 |

177301.55 |

3.0 |

9.0 |

6.0 |

0.94 |

|

GUAAC21-024 |

Guadium |

46230.96 |

177549.99 |

3.0 |

24.0 |

21.0 |

4.85 |

|

Including |

6.0 |

15.0 |

9.0 |

7.24 |

|||

|

KWHAC21-001 |

Kwahu |

56135.89 |

174434.90 |

45.0 |

51.0 |

6.0 |

1.96 |

|

KWHAC21-002 |

Kwahu |

56117.32 |

174454.69 |

18.0 |

21.0 |

3.0 |

5.38 |

|

KWHAC21-002 |

Kwahu |

56117.32 |

174454.69 |

30.0 |

36.0 |

6.0 |

4.98 |

|

KWHAC21-002 |

Kwahu |

56117.32 |

174454.69 |

51.0 |

54.0 |

3.0 |

2.48 |

|

KWHAC21-005 |

Kwahu |

56011.24 |

174676.77 |

6.0 |

15.0 |

9.0 |

1.76 |

|

KWHAC21-005 |

Kwahu |

56011.24 |

174676.77 |

18.0 |

21.0 |

3.0 |

1.41 |

|

KWHAC21-007 |

Kwahu |

56040.50 |

174645.79 |

48.0 |

51.0 |

3.0 |

1.08 |

|

ABSAC21-005 |

Abada |

44929.77 |

175587.56 |

9.0 |

21.0 |

12.0 |

1.01 |

|

ABSAC21-006 |

Abada |

44925.02 |

175546.52 |

45.0 |

54.0 |

9.0 |

1.13 |

Though the geometry of the mineralized trends is yet to be determined, initial results from the air core program have been encouraging with strong targets for follow up being generated. The highlights include:

- GUAAC21-024 (Guadium) on section 46225N, testing >200ppb gold in soil anomaly, intercepted 21.0 metres at 4.85g/t at surface. Follow-up drilling will be designed to test the down-dip and strike extensions of the intersection.

- KWHAC-002 (Kwahu) on section L3, intercepting 6.0 metres at 4.98 g/t, drilled c.35m below BERB443, on same section, which intersected 5.0 metres at 4.0g/t. This intersection is further confirmation of the down-dip extension of the mineralized structure at Kwahu, which remains open.

FINANCIAL PERFORMANCE SUMMARY

Please refer to the Company's condensed interim consolidated financial statements and related notes for the three and six months ended June 30, 2021 and related Management's Discussion and Analysis for the detailed discussion on the financial results for the three and six months ended June 30, 2021.

Table 6 – Financial Performance Summary (continuing operations) - Three and six months ended June 30, 2021

|

1. See "Non-GAAP Financial Measures" |

Q2 2021 |

Q2 2020 |

% change |

H1 2021 |

H1 2020 |

% change |

|

|

Realized gold price - spot sales |

$/oz |

1,807 |

1,713 |

5% |

1,793 |

1,645 |

9% |

|

Realized gold price - Streaming agreement2 |

$/oz |

792 |

836 |

(5)% |

788 |

823 |

(4)% |

|

Realized gold price – Consolidated |

$/oz |

1,709 |

1,621 |

5% |

1,688 |

1,559 |

8% |

|

Gold revenues |

$m |

64.4 |

75.4 |

(15)% |

129.4 |

129.5 |

- |

|

Cost of sales |

$m |

31.9 |

33.6 |

(5)% |

63.3 |

59.6 |

6% |

|

Depreciation and amortization |

$m |

7.1 |

6.3 |

13% |

14.4 |

11.4 |

26% |

|

Mine operating profit |

$m |

25.5 |

35.5 |

(28)% |

51.7 |

58.5 |

(12)% |

|

Corporate general and administrative expense |

$m |

4.2 |

4.3 |

(2)% |

9.2 |

9.5 |

(3)% |

|

Exploration expense |

$m |

1.4 |

0.4 |

250% |

2.2 |

1.2 |

83% |

|

Share based compensation expense |

$m |

0.9 |

0.7 |

29% |

1.5 |

1.6 |

(6)% |

|

Other expenses, net |

$m |

17.7 |

(0.6) |

3,050% |

20.6 |

- |

- |

|

Loss/(Gain) on fair value of derivative financial instruments, net |

$m |

0.7 |

1.8 |

(61)% |

(6.5) |

(2.3) |

(183)% |

|

Income before finance and tax |

$m |

0.5 |

29.0 |

(98)% |

24.8 |

48.5 |

(49)% |

|

EBITDA |

$m |

7.6 |

35.2 |

(78)% |

39.2 |

59.9 |

(35)% |

|

Adj. EBITDA |

$m |

26.0 |

36.4 |

(28)% |

53.3 |

57.6 |

(8)% |

|

Finance Expense, net |

$m |

1.0 |

3.3 |

(70)% |

4.7 |

6.9 |

(32)% |

|

Tax expense |

$m |

10.0 |

14.0 |

(29)% |

19.7 |

22.2 |

(11)% |

|

Net (loss)/income from continuing operations |

$m |

(10.4) |

11.7 |

(189)% |

0.4 |

19.4 |

(98)% |

|

Net (loss)/income per share attributable to shareholders |

$/share |

(0.11) |

0.08 |

(238)% |

(0.03) |

0.14 |

(121)% |

|

Adj. income per share attributable to shareholders - basic1 |

$/share |

0.05 |

0.10 |

(50)% |

0.09 |

0.12 |

(25)% |

|

Cash provided by operations before working capital |

$m |

23.2 |

34.9 |

(34)% |

46.5 |

52.1 |

(11)% |

|

Changes in working capital and taxes paid |

$m |

(10.3) |

(4.0) |

(158)% |

(23.3) |

(13.5) |

(73)% |

|

Net cash used in investing activities |

$m |

(10.4) |

(9.6) |

(8)% |

(23.2) |

(22.0) |

(5)% |

|

Net cash provided by financing activities |

$m |

4.2 |

(5.6) |

175% |

11.9 |

(5.5) |

316% |

|

Free cash flow |

$m |

2.4 |

21.4 |

(89)% |

- |

16.5 |

(100)% |

|

Notes: |

|

|

Discussion on Q2 2021 Financials

- Realized gold price - Including the unwinding of the deferred revenue from the streaming agreement with RGLD Gold AG (the "RGLD Streaming Agreement"), the realized gold price averaged $1,709/oz. The realized gold price for spot sales of $1,807/oz in Q2 2021 compared favorably to the $1,713/oz achieved in Q2 2020.

- Revenue totaled $64.4m in Q2 2021, 15% lower than $75.4m in Q2 2020 due to lower gold sales, in part offset by a 5% increase in the average realized gold price.

- Depreciation increased to $7.1m for Q2 2021 compared to $6.3m for Q2 2020 mainly due to the higher capital cost base following the completion of the infrastructure projects at the end of full year 2020. Depreciation is expected to continue at this elevated level and increase in line with the production rate.

- Corporate general and administrative expense amounted to $4.2m in Q2 2021 compared to $4.3m in the same period in 2020 and amounted to $9.2m for H1 2021 compared to $9.5m for the same period in 2020. The first four months in 2020 marked the relocation of the corporate office from Toronto, Canada to London, United Kingdom resulting in the Company incurring one-off associated costs. The reduction in staff costs, travel, consulting fees and recruitment costs in 2021 is partly offset by higher insurance costs.

- Loss on fair value of derivative financial liabilities totaled $0.7m during Q2 2021, this included:

- Hedging - During Q2 2021, a number of the original hedge contracts matured with no realized losses associated with the contracts during Q4 2020, however, the Company recognized an unrealized loss of $0.9m during the quarter. At the end of Q2 2021, these zero cost collars consist of puts and calls on 150koz maturing at a quarterly rate of 12.5koz. All hedges have a floor of $1,600/oz and an average ceiling of $2,171/oz in 2021 and $2,179/oz in 2022 and a flat ceiling of $2,115/oz in 2023 and 2024.

- 7% Convertible Debentures - A gain of $0.2m was recorded during the quarter. The Convertible Debentures mature in August 2021 and the Company intends to repay the facility using its current cash and available liquidity.

- EBITDA (see "Non-GAAP Financial Measures") from continuing operations amounted to $7.6m for Q2 2021 (Q2 2020 $35.2m).

- Adjusted EBITDA totaled $26m, representing a decrease of 28% compared to Q2 2020. The decrease in Adjusted EBITDA was primarily due to lower production volumes resulting in lower revenues, increased mine operating costs and increased exploration expenses. The adjustments applied include:

- The loss on fair value of financial instruments of $0.7m

- Other expenses of $17.7m. This is mainly comprised of a non-cash loss allowance recognized on the deferred consideration for the sale of Prestea of $17.4 million was recognized in Q2 2021

- Adjusted net income attributable to Golden Star shareholders (see "Non-GAAP Financial Measures" section) was $6.1m or $0.05 basic income per share in Q2 2021 compared to $9.5m or $0.09 basic income per share in Q2 2020. This was impacted by the lower gold sales and a higher depreciation charge during the quarter. Adjusted net income attributable to Golden Star shareholders reflects adjustments for non-recurring and abnormal items which are mostly non-cash in nature, including:

- The loss on fair value of financial instruments of $0.7m

- Loss allowance on deferred consideration on the sale of Prestea $17.4m

- Working capital and taxes paid - The working capital balance increased during Q2 2021 resulting in a cash outflow of $5m. In addition, $5.4m of income tax liabilities, relating to Q1 2021, were paid during Q2 2021.

- Investing activities - Net cash used in investing activities totaled $10.4m which includes the following cash flows:

- Capital expenditures of $12.2m

- Change in accounts payable and deposits on mine equipment and material $1.8m which relates to an increase in accruals for capital investments during the quarter

- Net cash from financing activities totaled $4.2m. This includes the $5.2m of net proceeds from the ATM Program received during the quarter.

- Free cash flow - During Q2 2021, continuing operations generated $2.4m of free cash flow, despite the significant working capital outflow during the quarter of $10.3m and capital investment of $12.2m.

Financial position

The Company held $72.7m of cash and cash equivalents and $103.7m of debt, for net debt of $31m as at June 30, 2021. The net debt position improved by $8.5m during Q2 2021 as a result of the $6.6m increase in the cash position following the use of the ATM Program during the quarter. The table below summarizes the financial position of the Company:

Table 7 – Financial Position - Three months ended March 31, 2021

|

Q2 2021 |

Q2 2020 |

% change |

||

|

Summary of debt facilities |

||||

|

Macquarie Credit Facility |

$m |

52.5 |

52.8 |

1% |

|

Convertible Debentures |

$m |

51.2 |

48.3 |

6% |

|

Gross Debt Position |

$m |

103.7 |

101.1 |

3 |

|

Cash Position |

$m |

72.7 |

45.1 |

61% |

|

Net Debt |

$m |

31.0 |

56.0 |

(45)% |

Company Profile:

Golden Star is an established gold mining company that owns and operates the Wassa underground mine in Ghana, West Africa. Listed on the NYSE American, the Toronto Stock Exchange and the Ghana Stock Exchange, Golden Star is focused on delivering strong margins and free cash flow from the Wassa mine. As the winner of the Prospectors & Developers Association of Canada 2018 Environmental and Social Responsibility Award, Golden Star remains committed to leaving a positive and sustainable legacy in its areas of operation.

Statements Regarding Forward-Looking Information

Some statements contained in this news release are "forward-looking statements" within the meaning of the Private Securities Litigation Reform Act of 1995 and "forward looking information" within the meaning of Canadian securities laws. Forward looking statements and information include but are not limited to, statements and information regarding: present and future business strategies and the environment in which Golden Star will operate in the future, including the price of gold, anticipated costs and ability to achieve goals; gold production, cash operating costs, production and cost guidance; capital and exploration expenditure guidance; the ability to expand the Company and its production profile through the exploration and development of its existing mine; expected grade and mining rates for 2021; the sources of gold production at Wassa Underground for the remainder of 2021; estimated costs and timing of the development of new mineral deposits and sources of funding for such development; the anticipated delivery of ore pursuant to delivery obligations under the RGLD Streaming Agreement; the use of proceeds from the Sales Agreement; receipt of payment and timing of the deferred consideration pursuant to the terms of the SPA; RGLD's continued investment in the Golden Star oil palm plantations; the processing of low grade stockpiles at Wassa; Wassa production contribution from stockpiles and the processing grade thereof for the remainder of 2021; expectations regarding the sustainability of current gold prices; implementation of exploration programs at Wassa and the timing thereof; the acceleration of the growth and development of the resource base at Wassa; the investment in drilling and development in 2021 resulting in increased mining rates; the nature, scope and timing of in-mine exploration activities at Wassa; the timing for the evaluation of the first phase drilling results at Wassa near mine; the generation and identification of targets for follow up drilling in and around HBB; the ability to identify opportunities to further expand Golden Star's business; the ability to materially increase production at Wassa through development capital investments; the use of the non-hedge gold collar contracts; the delivery of a range of operational initiatives that improve the consistency of the operations and visibility of the longer-term potential of the operations; the life of mine; the timing for rehabilitation work and the expected discounted rehabilitation costs; the ability of the Company to repay the 7% Convertible Debentures when due or to restructure them or make alternate arrangements; the term of the RCF and the step down in capacity; the securing of adequate supply chains for key consumables and potential delays in the supply chain; the Company having sufficient cash available to support its operations and mandatory expenditures for the next 12 months; the continued commissioning process for the new paste plant; the introduction of second stopes planned for mining; the Company increasing exploration activities; planned exploration at Wassa and the timing and budget thereof; the ability to continue as a going concern; the effectiveness of internal controls; the potential impact of a disruption in Wassa's operations; the ability to generate strong margins and sufficient free cash flow, raise additional financing or establish refinancing options for the Company's current debt; the continued ATM Program from time-to-time; the timing, duration and overall impact of the COVID-19 pandemic on the Company's operations and the ability to mitigate such impact; the quantum of cash flow from the sale of Prestea and the anticipated receipt and timing thereof; the outcome of the Prestea Severance Claim, and the timing for the settlement of the record, preparation of the record and transmission of the record of appeal to the Court of Appeal of Ghana related thereto; the availability of mineral reserves based on the accuracy of the Company's updated mineral reserve and resource models; planned drilling activities; the ability to convert mineral resources to mineral reserves through the planned infill drilling program; the potential to increase the Company's mineral resources outside of its existing mineral resources footprint; the anticipated impact of increased exploration on current mineral resources and mineral reserves; identification of acquisition and growth opportunities; relationships with local stakeholder communities; and the potential incurrence of further debt in the future.. Generally, forward-looking information and statements can be identified by the use of forward-looking terminology such as "plans", "expects", "is expected", "budget", "scheduled", "estimates", "forecasts", "intends", "anticipates", "believes" or variations of such words and phrases (including negative or grammatical variations) or statements that certain actions, events or results "may", "could", "would", "might" or "will be taken", "occur" or "be achieved" or the negative connotation thereof. Investors are cautioned that forward-looking statements and information are inherently uncertain and involve risks, assumptions and uncertainties that could cause actual facts to differ materially. Such statements and information are based on numerous assumptions regarding present and future business strategies and the environment in which Golden Star will operate in the future. Forward-looking information and statements are subject to known and unknown risks, uncertainties and other important factors that may cause the actual results, performance or achievements of Golden Star to be materially different from those expressed or implied by such forward-looking information and statements, including but not limited to: gold price volatility; discrepancies between actual and estimated production; mineral reserves and resources and metallurgical recoveries; mining operational and development risks; liquidity risks; suppliers suspending or denying delivery of products or services; regulatory restrictions (including environmental regulatory restrictions and liability); actions by governmental authorities; the speculative nature of gold exploration; ore type; the global economic climate; share price volatility; the availability of capital on reasonable terms or at all; risks related to international operations, including economic and political instability in foreign jurisdictions in which Golden Star operates; risks related to current global financial conditions; actual results of current exploration activities; environmental risks; future prices of gold; possible variations in mineral reserves and mineral resources, grade or recovery rates; mine development and operating risks; an inability to obtain power for operations on favourable terms or at all; mining plant or equipment breakdowns or failures; an inability to obtain products or services for operations or mine development from vendors and suppliers on reasonable terms, including pricing, or at all; public health pandemics such as COVID-19, including risks associated with reliance on suppliers, the cost, scheduling and timing of gold shipments, uncertainties relating to its ultimate spread, severity and duration, and related adverse effects on the global economy and financial markets; accidents, labor disputes and other risks of the mining industry; delays in obtaining governmental approvals or financing or in the completion of development or construction activities; litigation risks; and risks related to indebtedness and the service of such indebtedness. Although Golden Star has attempted to identify important factors that could cause actual results to differ materially from those contained in forward-looking information and statements, there may be other factors that cause results not to be as anticipated, estimated or intended. There can be no assurance that future developments affecting the Company will be those anticipated by management. Please refer to the discussion of these and other factors in management's discussion and analysis of financial conditions and results of operations for the year ended December 31, 2020, and in our annual information form for the year ended December 31, 2019 as filed on SEDAR at www.sedar.com. The forecasts contained in this press release constitute management's current estimates, as of the date of this press release, with respect to the matters covered thereby. We expect that these estimates will change as new information is received. While we may elect to update these estimates at any time, we do not undertake any estimate at any particular time or in response to any particular event.

Technical Information

The technical contents of this press release have been reviewed and approved by S. Mitchel Wasel, BSc Geology, a Qualified Person pursuant to National Instrument 43-101. Mr. Wasel is Vice President of Exploration for Golden Star and an active member and Registered Chartered Professional of the Australasian Institute of Mining and Metallurgy.

The results for Wassa drilling stated herein are based on the analysis of saw-split HQ/NQ diamond half core or a three kilogram single stage riffle split of a nominal 25 to 30 kg Reverse Circulation chip sample which has been sampled over nominal one metre intervals (adjusted where necessary for mineralized structures). Sample preparation and analyses have been carried out at Intertek Laboratories in Tarkwa, which are independent from Golden Star, using a 1,000 gram slurry of sample and tap water which is prepared and subjected to an accelerated cyanide leach (LEACHWELL). The sample is then rolled for twelve hours before being allowed to settle. An aliquot of solution is then taken, gold extracted into Di-iso Butyl Keytone (DiBK), and determined by flame Atomic Absorption Spectrophotometry (AAS). Detection Limit is 0.01 ppm.

All analytical work is subject to a systematic and rigorous Quality Assurance-Quality Control (QA-QC). At least 5% of samples are certified standards and the accuracy of the analysis is confirmed to be acceptable from comparison of the recommended and actual "standards" results. The remaining half core is stored on site for future inspection and detailed logging, to provide valuable information on mineralogy, structure, alteration patterns and the controls on gold mineralization.

Non-GAAP Financial Measures

In this press release, we use the terms "cash operating cost", "cash operating cost per ounce", "all-in sustaining costs", "all-in sustaining costs per ounce", "adjusted net (loss)/income attributable to Golden Star shareholders", "adjusted (loss)/income per share attributable to Golden Star shareholders", "cash provided by operations before working capital changes", and "cash provided by operations before working capital changes per share - basic".

"Cost of sales excluding depreciation and amortization" as found in the statements of operations includes all mine-site operating costs, including the costs of mining, ore processing, maintenance, work-in-process inventory changes, mine-site overhead as well as production taxes, royalties, severance charges and by-product credits, but excludes exploration costs, property holding costs, corporate office general and administrative expenses, foreign currency gains and losses, gains and losses on asset sales, interest expense, gains and losses on derivatives, gains and losses on investments and income tax expense/benefit.

"Cost of sales per ounce" is equal to cost of sales excluding depreciation and amortization for the period plus depreciation and amortization for the period divided by the number of ounces of gold sold (excluding pre-commercial production ounces sold) during the period.

"Cash operating cost" for a period is equal to "cost of sales excluding depreciation and amortization" for the period less royalties, the cash component of metals inventory net realizable value adjustments, materials and supplies write-off and severance charges, and "cash operating cost per ounce" is that amount divided by the number of ounces of gold sold (excluding pre-commercial production ounces sold) during the period. We use cash operating cost per ounce as a key operating metric. We monitor this measure monthly, comparing each month's values to prior periods' values to detect trends that may indicate increases or decreases in operating efficiencies. We provide this measure to investors to allow them to also monitor operational efficiencies of the Company's mines. We calculate this measure for both individual operating units and on a consolidated basis. Since cash operating costs do not incorporate revenues, changes in working capital or non-operating cash costs, they are not necessarily indicative of operating profit or cash flow from operations as determined under IFRS. Changes in numerous factors including, but not limited to, mining rates, milling rates, ore grade, gold recovery, costs of labor, consumables and mine site general and administrative activities can cause these measures to increase or decrease. We believe that these measures are similar to the measures of other gold mining companies, but may not be comparable to similarly titled measures in every instance.

"All-in sustaining costs" commences with cash operating costs and then adds the cash component of metals inventory net realizable value adjustments, royalties, sustaining capital expenditures, corporate general and administrative costs (excluding share-based compensation expenses and severance charges), and accretion of rehabilitation provision. For mine site all-in sustaining costs, corporate general and administrative costs (excluding share-based compensation expenses and severance charges) are allocated based on gold sold by each operation. "All-in sustaining costs per ounce" is that amount divided by the number of ounces of gold sold (excluding pre-commercial production ounces sold) during the period. This measure seeks to represent the total costs of producing gold from current operations, and therefore it does not include capital expenditures attributable to projects or mine expansions, exploration and evaluation costs attributable to growth projects, income tax payments, interest costs or dividend payments. Consequently, this measure is not representative of all of the Company's cash expenditures. In addition, the calculation of all-in sustaining costs does not include depreciation expense as it does not reflect the impact of expenditures incurred in prior periods. Therefore, it is not indicative of the Company's overall profitability. Share-based compensation expenses are also excluded from the calculation of all-in sustaining costs as the Company believes that such expenses may not be representative of the actual payout on equity and liability based awards.

The Company believes that "all-in sustaining costs" will better meet the needs of analysts, investors and other stakeholders of the Company in understanding the costs associated with producing gold, understanding the economics of gold mining, assessing the operating performance and the Company's ability to generate free cash flow from current operations and to generate free cash flow on an overall Company basis. Due to the capital intensive nature of the industry and the long useful lives over which these items are depreciated, there can be a disconnect between net earnings calculated in accordance with IFRS and the amount of free cash flow that is being generated by a mine. In the current market environment for gold mining equities, many investors and analysts are more focused on the ability of gold mining companies to generate free cash flow from current operations, and consequently the Company believes these measures are useful non-IFRS operating metrics ("non-GAAP measures") and supplement the IFRS disclosures made by the Company. These measures are not representative of all of Golden Star's cash expenditures as they do not include income tax payments or interest costs. Non-GAAP measures are intended to provide additional information only and do not have standardized definitions under IFRS and should not be considered in isolation or as a substitute for measures of performance prepared in accordance with IFRS. These measures are not necessarily indicative of operating profit or cash flow from operations as determined under IFRS.

"Adjusted net (loss)/income attributable to Golden Star shareholders" is calculated by adjusting net (loss)/income attributable to Golden Star shareholders for (gain)/loss on fair value of financial instruments, share-based compensation expenses, severance charges, loss/(gain) on change in asset retirement obligations, deferred income tax expense, non-cash cumulative adjustment to revenue and finance costs related to the Streaming Agreement, and impairment. The Company has excluded the non-cash cumulative adjustment to revenue from adjusted net income/(loss) as the amount is non-recurring, the amount is non-cash in nature and management does not include the amount when reviewing and assessing the performance of the operations. "Adjusted (loss)/income per share attributable to Golden Star shareholders" for the period is "Adjusted net (loss)/income attributable to Golden Star shareholders" divided by the weighted average number of shares outstanding using the basic method of earnings per share.

For additional information regarding the Non-GAAP financial measures used by the Company, please refer to the heading "Non-GAAP Financial Measures" in the Company's Management Discussion and Analysis of Financial Condition and Results of Operations for the year ended December 31, 2020 and the three months ended March 31, 2021, which are available at www.sedar.com.

![]() View original content to download multimedia:https://www.prnewswire.com/news-releases/golden-star-resources-reports-results-for-the-three-and-six-months-ended-june-30-2021-301343594.html

View original content to download multimedia:https://www.prnewswire.com/news-releases/golden-star-resources-reports-results-for-the-three-and-six-months-ended-june-30-2021-301343594.html

SOURCE Golden Star Resources Ltd.